Nobody Sits Down and Decides to Waste $200 a Month

It happens gradually. One streaming service because everyone was talking about a show. A gym membership in January when motivation was high. A meditation app that seemed worth it for three weeks. A cloud storage upgrade because your phone ran out of space. A news subscription for one article you wanted to read.

Each one made sense at the time. Each one was a small, reasonable decision. And then life moved on and the decisions stayed, billing quietly every month whether you used the service or not.

This is the subscription trap. Not one bad decision but a hundred small ones that accumulate into a significant monthly drain that most people do not notice because no single charge is large enough to trigger alarm.

The average person now has more recurring charges than at any point in history. Subscription business models have exploded over the last decade precisely because they are so effective at generating passive revenue from customers who signed up once and never actively chose to continue. The burden of action is on you to cancel. If you do nothing, they keep charging.

This article is about doing something about it. Specifically, how to find every subscription you are paying for, how to decide which ones are worth keeping, and how to actually cancel the ones that are not, including the ones that make cancellation deliberately difficult.

Why Subscriptions Are Designed to Be Invisible

Understanding why this happens makes it easier to fix.

Subscription companies spend significant resources on what the industry calls reducing churn, which is the rate at which customers cancel. Every friction point between you and cancellation is intentional. The button that is hard to find. The “are you sure?” screen followed by a special offer. The requirement to call a phone number during business hours to cancel a service you signed up for online in 30 seconds. The annual billing that means the charge only appears once and is easy to forget about.

Beyond cancellation friction, there is the billing name problem. Many subscriptions appear on your statement under a parent company name rather than the product name you recognise. A charge from “ADOBE SYSTEMS” might be Creative Cloud. “NFLX” is Netflix. “AMZN DIGITAL” could be Amazon Prime, Kindle Unlimited, Amazon Music, or Audible, or all four separately. When the name is not immediately recognisable you are less likely to investigate and more likely to scroll past.

Annual subscriptions are especially effective at staying invisible. You sign up, forget, and the annual charge hits your card 11 months later when you are no longer thinking about it. By then the service has become a background assumption rather than an active choice.

Knowing these mechanics does not make you immune to them. But it does mean that when you are going through your statements and feel the urge to skip past a charge because it is familiar or small, you catch yourself.

Step 1: The Full Statement Pull

Go back three months on both your bank account and every credit card you use. Do not do this from memory. Do not approximate. Pull the actual statements.

Go line by line. Every single charge. For each one, write down the name, the amount, and whether it recurs.

Do not make any decisions yet. Just make the list. This is data collection, not judgment. People make better decisions when they have the full picture first rather than cancelling things reactively as they find them.

Pay specific attention to:

Charges under $20. These are the ones most likely to go unnoticed. A $6.99 charge, a $9.99 charge, a $14.99 charge. They feel trivial individually. Eight of them together is $90 per month, which is $1,080 per year.

Charges you cannot immediately name. Write them down anyway and look them up. Go to your browser and search the exact charge name that appears on your statement followed by the word “subscription” or “billing.” You will almost always find out what it is within 30 seconds.

Charges that appear annually. These are easy to miss in a monthly scan. Look for any charge that is significantly larger than typical and appeared only once in your three-month window.

Charges from food delivery, takeaway, or meal kit services. These often include a membership or subscription component that runs separately from your individual orders.

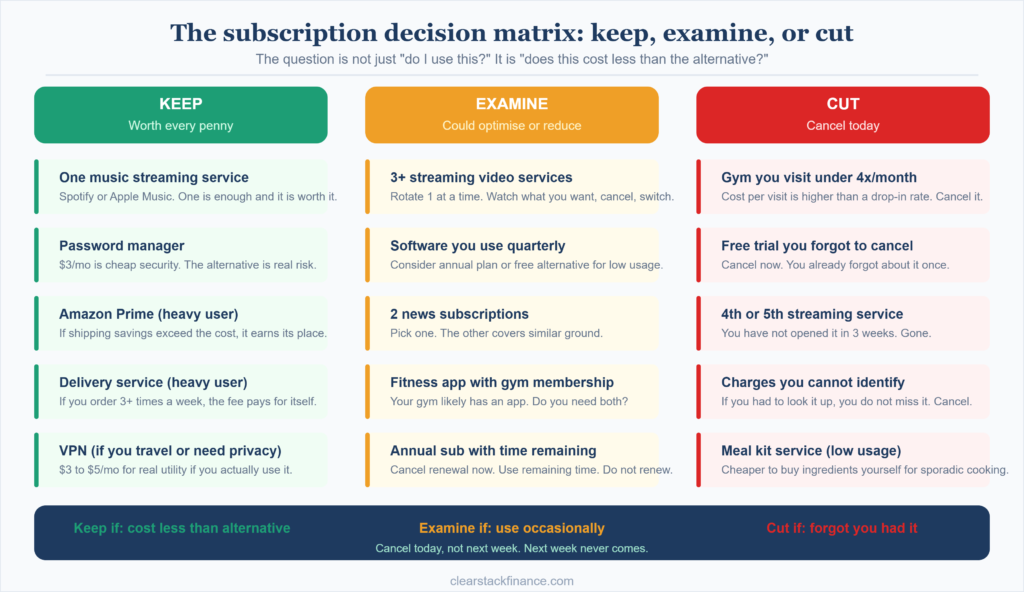

Step 2: Categorise What You Find

Once you have the full list, sort each subscription into one of three categories.

The first category is genuinely use and value. These are services you actively use, would notice if they disappeared, and consider worth the cost relative to what you spend. These stay.

The second category is use occasionally but could reduce. A streaming service you watch maybe twice a month. A software tool you use a few times a year. A news subscription you read sporadically. These are worth examining more carefully. Could you share a plan with someone to halve the cost? Could you subscribe for three months per year when you actually use it and cancel for the rest? Could you downgrade to a cheaper tier?

The third category is not using or barely using. These cancel immediately. Not next week. Not after you finish the series you started. Today.

Most people doing this for the first time find their list breaks down roughly into 40% keep, 30% examine, and 30% cancel. That 30% cancel category alone typically represents $40 to $120 per month depending on how many subscriptions have accumulated.

Step 3: The Actual Cancellation Process

This is where most guides stop, which is unhelpful because cancellation is often where things get complicated.

For straightforward online cancellations, go to the account settings of the service, find the subscription or billing section, and cancel from there. Do this now, while you have the statement in front of you and the motivation is fresh. Do not add it to a to-do list. A to-do list is where cancellations go to die.

For services that require a phone call, which is a deliberate friction tactic used commonly by gyms, cable providers, and some insurance companies, here is the script that works:

Call the customer service number. When the agent answers, say: “I would like to cancel my membership effective immediately. My account details are [give your details]. I do not need to hear about any retention offers, I have made my decision. Can you confirm the cancellation and send me a confirmation email?”

The key elements of that script are confirming you do not want retention offers before they pitch them, asking for written confirmation, and stating you want the cancellation effective immediately rather than at the end of the billing period if possible.

Some gyms specifically require in-person cancellation or certified mail. If you encounter this, send the certified letter the same day. Gym contracts are heavily regulated in most Canadian provinces, US states, and UK consumer law, and there are limits on what they can require for cancellation. If a gym is making cancellation unreasonably difficult, check your provincial, state, or national consumer protection guidelines. In many cases they are legally required to cancel within a specified time frame once you have made a written request.

For annual subscriptions, cancel now even if there is time remaining on the current period. The service will typically remain active until the end of the paid period. What you are doing is ensuring it does not renew. Mark the cancellation date in your calendar as confirmation..

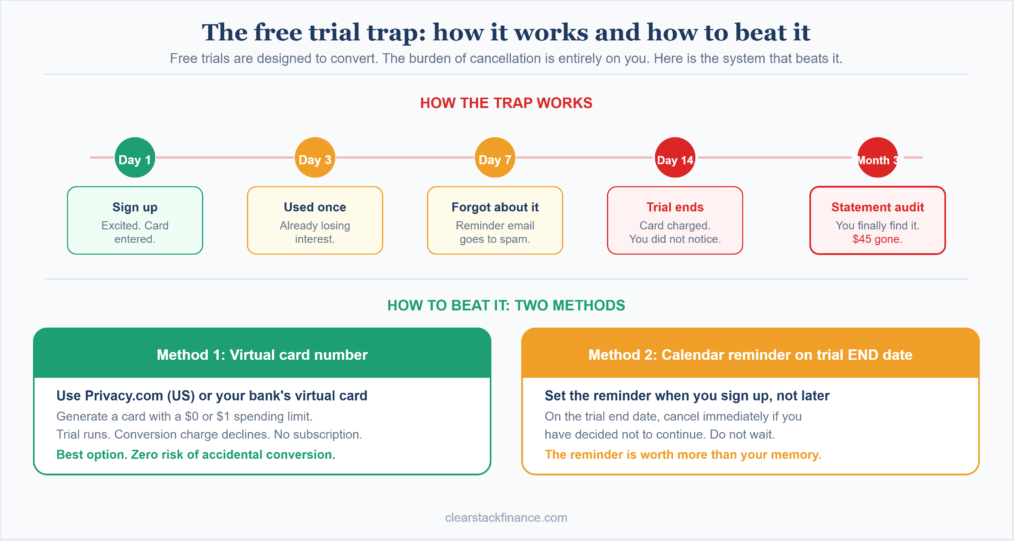

The Free Trial Problem

Free trials are worth mentioning separately because they are their own category of subscription trap.

A free trial requires a credit card to start. The trial ends and the service converts to paid automatically. You receive an email notification that is easy to miss or that goes to a folder you do not check. The charge appears on your next statement under a name you might not immediately recognise. Three months later you notice it and realise you have been paying for something you stopped thinking about two days after signing up.

The most effective approach if you want to use free trials: use a virtual card number if your bank offers them. Some Canadian banks and most major US banks through services like Privacy.com allow you to generate a virtual card number with a spending limit. Set the limit to $0 or $1. The trial runs, the card declines when they try to charge it, the subscription does not convert.

If you do not have access to virtual cards, put a calendar reminder on the day the trial ends, not the day you sign up. That reminder is the only thing that consistently prevents automatic conversion.

Subscriptions Worth Keeping: How to Actually Decide

The question most people ask when looking at their subscription list is: do I use this? That is the wrong question.

The right question is: does this cost less than the alternative?

Spotify at $11 per month versus buying music individually. Amazon Prime at $10 per month if you order regularly enough that the free shipping alone covers the cost. A password manager at $3 per month versus the security risk and time cost of not having one.

Some subscriptions are worth keeping even with relatively low usage if the alternative is significantly more expensive or significantly less convenient. The analysis is cost versus alternative, not just usage frequency.

The subscriptions that almost never survive honest analysis are the ones where the alternative is simply doing without. A fourth streaming service when you already have three. A second news subscription covering the same topics as the first. A fitness app you already have through your phone’s built-in health tracking. A cloud storage upgrade that could be solved by deleting photos you have not looked at in four years.

After You Cancel: The Three Month Check

Cancellation confirmation does not always mean the billing actually stopped. This happens more often than it should, particularly with services that use third-party billing processors or that have complicated account structures.

Three months after your cancellation audit, pull your statements again and check that every cancelled subscription has actually stopped appearing. If a charge continues after you cancelled, you have grounds for a refund and the service is legally required to process it in most jurisdictions. Contact your bank if the service does not cooperate, as most banks will initiate a chargeback for charges that continued after a confirmed cancellation.

Also check that any services you downgraded are billing at the lower tier rather than the original amount. Billing system errors after plan changes are surprisingly common.

READ ALSO: I Started Investing at 26 With $100, Made Every Mistake Possible. This Is What I Learned

The Accumulation Problem Does Not Go Away

Here is the honest part. You will do this audit, cancel what you should cancel, feel good about it, and then over the next 12 months new subscriptions will gradually accumulate again.

A new service launches and you sign up for a trial. An app you download has a premium tier you upgrade to. A service you cancelled gets a new feature that pulls you back. This is normal and it is not a failure of willpower. It is just how subscription services are designed to work.

The solution is not to never subscribe to anything. It is to run this audit every three to four months rather than treating it as a one-time event. A quarterly subscription sweep takes 20 minutes once you have done it the first time because you already know your baseline. You are just looking for what has accumulated since the last pass.

Set a calendar reminder right now. Three months from today. Call it subscription check. That reminder is worth several hundred dollars per year in prevented accumulation.

What This Actually Adds Up To

Running a full subscription audit and cancelling what should be cancelled typically recovers $50 to $150 per month for someone who has never done it before.

That is $600 to $1,800 per year. Not from earning more. Not from cutting things you value. From stopping payments for things you had already forgotten you were making.

The time investment is about 90 minutes for the first full audit. After that, the quarterly check takes 20 minutes. The hourly return on those 90 minutes is one of the highest you will find in personal finance.

Heads up: Nothing in this article is financial advice and I am not a financial advisor. Subscription terms, cancellation policies, and consumer protection laws vary by country and provider. Always check the specific terms of any service you are cancelling and verify your rights under local consumer protection legislation if you encounter difficulty.

READ ALSO: How to Cut Your Grocery Bill by $150 a Month Without Eating Differently

Mike is a data analyst based in Niagara Falls, Ontario. He started ClearStack Finance after spending years figuring out personal finance the hard way. No financial jargon, no boring lectures, just practical money advice for people in their 20s and 30s who are still figuring it out.