Most People Have No Idea Where Their Money Actually Goes

Not because they are careless. Because modern spending is designed to be invisible.

Twelve years ago, losing track of your money meant forgetting about cash you spent. Today it means forgetting about the Netflix subscription you share with someone who moved out two years ago, the gym membership you use twice a month but feel too guilty to cancel, the app subscription that renewed automatically at 3am on a Tuesday, and the insurance premium that quietly went up $18 last October and you never noticed.

None of these are dramatic. None of them feel like a big deal individually. But they stack.

The average person in their 20s and 30s has between 8 and 12 active subscriptions at any given time according to research from C+R Research. The average American household spends $273 per month on subscriptions alone, and most people when surveyed estimate they spend about $80. That is a gap of nearly $200 per month on a single category, and most people have no idea it exists.

A monthly money audit is not a budget. It is not a spending plan. It is a diagnostic. You run it once, find out where money is quietly leaving your account, make a few decisions, and then you are done. The whole thing takes about an hour.

Here is exactly how to do it.

What You Actually Need to Start

Nothing complicated. You need access to three months of bank statements and three months of credit card statements. Download them as PDFs or just open them in your banking app.

You also need about an hour of uninterrupted time. Not 20 minutes. An hour. The first time through takes longer because you are building a picture of your spending from scratch. After that, a quarterly audit takes about 20 minutes.

Grab a notebook or open a spreadsheet. You are going to make a list as you go through the statements, not a budget, just a categorized list of where money went. The categories do not need to be fancy. Housing, transport, food, subscriptions, insurance, debt payments, personal spending, and everything else covers most of it.

Do not try to do this from memory. Memory is not reliable for spending. People consistently underestimate how much they spend on dining out, entertainment, and subscriptions by 30 to 50 percent. The statements do not lie.

Step 1: The Subscription Sweep

Go through your last three bank and credit card statements specifically looking for recurring charges. Anything that appears more than once, regardless of the amount.

Make a list of every single one. The amount, the name, and whether you actively use it.

Here is what you are looking for specifically:

Streaming services. Most people have more than they think. Netflix, Disney Plus, Amazon Prime, Spotify, Apple TV Plus, Crave, BBC iPlayer premium, YouTube Premium, and Paramount Plus are all common. Each one individually is $10 to $20 per month. Four of them together is $50 to $70.

Software and app subscriptions. Adobe Creative Cloud, Microsoft 365, Dropbox, iCloud storage, Google One, LastPass, Grammarly, Duolingo Plus, and dozens of others. These are easy to forget because they often bill annually and show up as one larger charge.

Gym and fitness memberships. Gyms are famous for making cancellation deliberately difficult. If you have not been in three months, this is the audit that makes you deal with it.

Delivery service subscriptions. DoorDash DashPass, Uber One, Amazon Fresh, HelloFresh, and similar services. Some of these are worth it if you use them constantly. Most people do not use them constantly.

News and media subscriptions. The New York Times, The Globe and Mail, The Guardian, Spotify Podcasts, and others. Individually small, collectively meaningful.

Insurance policies you have not reviewed. Car insurance, tenant or home insurance, life insurance, and extended warranties all tend to go up quietly at renewal without triggering any action.

Write down everything. Do not make decisions yet. Just get the full picture first.

Step 2: The Dining and Takeaway Reality Check

This one is uncomfortable for most people.

Add up every restaurant, takeaway, delivery, and coffee purchase across your last three months. Every single one. Then divide by three to get your monthly average.

The national average for dining out in Canada is about $200 to $300 per month per person according to Statistics Canada. In the US, the Bureau of Labor Statistics puts average food-away-from-home spending at around $3,000 per year for an individual, which is $250 per month. For couples or households it goes significantly higher.

The number most people find is higher than what they expected. Often significantly higher.

The point of this step is not to make you feel bad about enjoying food. It is to make the spending visible so you can make a conscious choice about it rather than a default one. There is a difference between deciding to spend $280 per month on dining out because you value it and you have accounted for it, and discovering you have been spending $280 per month on dining out without realizing it while wondering where your money goes.

After you have the real number, ask yourself one question: if you had seen this number before you spent it, would you have made the same choices? That question is more useful than any budgeting rule.

Step 3: The Insurance and Bills Audit

Most people set up insurance policies and utility bills and then never look at them again. This is one of the most reliable sources of recoverable money in any audit.

Pull out your current premiums and rates for:

Car insurance. When did you last get a quote from a competing provider? In Canada, car insurance premiums vary significantly between providers for identical coverage. Switching providers or simply calling your current one with a competitor quote often produces an immediate reduction of $20 to $80 per month.

Home or tenant insurance. Same principle. Rates increase at renewal. Competing quotes take 15 minutes online and frequently reveal meaningful savings.

Phone plan. The mobile market in Canada, the US, and the UK has changed significantly in the last three years. MVNOs (Mobile Virtual Network Operators) in all three markets now offer plans with comparable coverage to major carriers at 30 to 60 percent lower prices. If you have been on the same plan for more than two years, you are almost certainly overpaying.

Internet. Bundle discounts and promotional rates expire without notice. Calling your internet provider and asking what their current retention offer is takes five minutes and regularly produces $15 to $30 per month in savings with no change in service.

Utilities. Switching to a different gas or electricity provider in deregulated markets like parts of Canada, the UK, and many US states is often possible and often cheaper. Worth 20 minutes of research if you have not checked in two years.

Step 4: The Forgotten Subscriptions

These are different from the regular subscription sweep. Forgotten subscriptions are the ones that appear on your statement under names you do not immediately recognize.

Go through your statements again and flag any charge you cannot immediately identify. Look up the company name if it is not obvious. You will almost certainly find at least one or two charges you genuinely cannot account for.

Common culprits: free trials that converted to paid without a clear reminder, app subscriptions that changed their billing name, annual charges from services you signed up for once and forgot about, and charges from services you cancelled but which continued billing due to a processing error.

These are not your fault. They are deliberately designed to be easy to miss. But finding and cancelling them is pure recovered money.

Step 5: The Spending Pattern Questions

After you have done the factual parts of the audit, there are three questions worth sitting with:

What am I paying for that I do not use? Not just subscriptions. Anything. Gym equipment sitting in a room, a storage unit full of things you have not opened in two years, a car you could replace with transit for less. These are not always obvious until you are looking at your full spending picture.

What am I spending on out of habit rather than genuine preference? The coffee you get every morning because you have always gotten it, not because it is particularly good or important to you. The premium grocery store you shop at because it is familiar, not because you prefer it. The expensive phone plan you have because upgrading felt easier than comparing options. Habit spending is not inherently bad. Invisible habit spending is.

Where am I paying for convenience I could reduce? Food delivery markups, express shipping on things that could wait, premium services that solve problems you could solve with 20 minutes of time instead of $15 per month. The audit is about making these visible, not eliminating all of them.

What Happens After the Audit

You will have a list. On that list will be things to cancel, things to renegotiate, and things to keep because they are genuinely worth it.

Work through the list in order of value. Start with the largest amounts first.

Cancellations are usually straightforward but some services make it deliberately difficult. Gyms often require in-person visits or certified letters to cancel. Some subscription services require you to navigate several screens before finding the actual cancel option. Go through each one and complete the cancellation rather than planning to do it later. Planning to cancel and actually cancelling are different things.

Renegotiations require a phone call in most cases. The script is simple: you have been a customer for a certain number of years, you have seen lower rates elsewhere, and you would like to know what they can offer before you switch. Insurance companies, internet providers, and phone carriers all have retention departments with authority to offer discounts that are not advertised publicly.

Keep a record of what you cancelled and what you renegotiated. Not to track it obsessively, just so you can check in three months that the cancellations actually processed and the lower rates actually appeared on your bill.

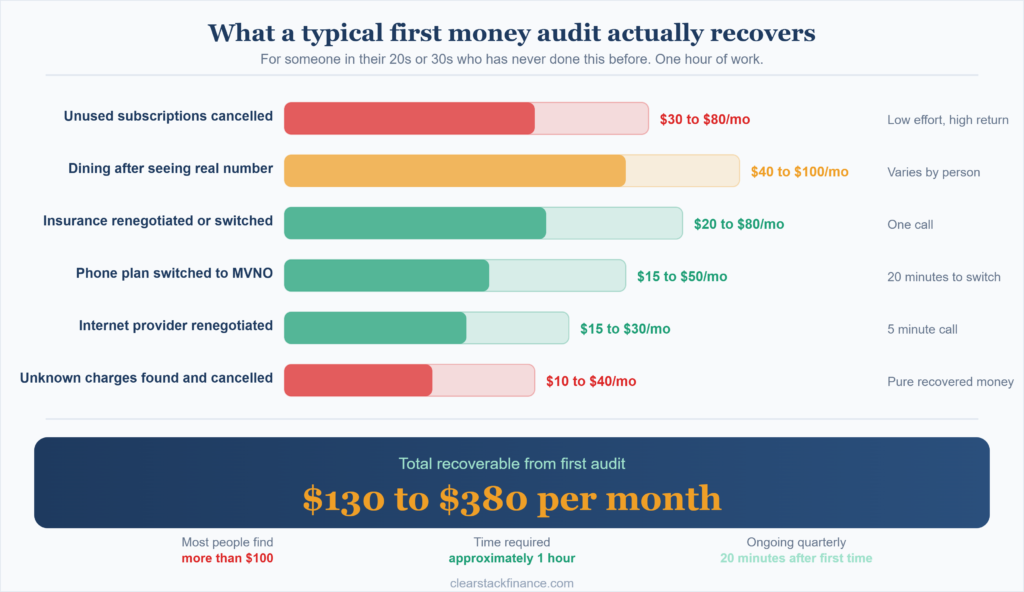

A Realistic Picture of What Most Audits Find

Based on the categories above, here is a rough picture of what a typical audit recovers for someone in their 20s or 30s who has not done this before:

Forgotten or unused subscriptions they cancel: $30 to $80 per month.

Dining and takeaway reduction after seeing the real number: $40 to $100 per month, depending on how far above their comfortable level the real number was.

Insurance renegotiation or switching: $20 to $80 per month.

Phone plan switch to a better value option: $15 to $50 per month.

Internet provider renegotiation: $15 to $30 per month.

Total recoverable: $120 to $340 per month for most people doing their first audit. Some people find more. Very few people who do this carefully find less than $100.

That money does not require earning more. It does not require cutting anything you genuinely value. It requires one hour of attention to where your money has already been going.

Do This Every Quarter, Not Just Once

Spending patterns drift. New subscriptions accumulate. Rates change. The audit that takes an hour the first time takes 20 minutes after that because you already know what you are looking for.

Set a calendar reminder for three months from now. Call it money audit. When it comes up, go through your statements again with the same checklist. You will catch the new things that accumulated in the previous three months before they become invisible habits.

The goal is not to be restrictive with money. The goal is to make sure every dollar leaving your account is doing something you actually chose.

Heads up: I am not a financial advisor and nothing here constitutes financial advice. The averages and statistics mentioned are for illustrative purposes. Always verify rates and figures with the relevant providers and official sources in your country.

Mike is a data analyst based in Niagara Falls, Ontario. He started ClearStack Finance after spending years figuring out personal finance the hard way. No financial jargon, no boring lectures, just practical money advice for people in their 20s and 30s who are still figuring it out.