The Number That Follows You Everywhere

Your credit score is one of those things that sits quietly in the background of your financial life until the moment it matters, and then it matters enormously.

It determines whether you get approved for an apartment. It affects the interest rate on your car loan, sometimes by several percentage points which over five years adds up to thousands of dollars. It comes up when you apply for a mortgage. Some employers in certain industries check it. Some insurance companies use it to set your premiums.

And yet most people have only a vague idea of what their score actually is, a vaguer idea of what goes into it, and almost no idea how to move it in the right direction beyond “pay your bills on time.”

That last part is true but incomplete. Paying on time is the foundation but it is not the whole picture. This article covers what your score is actually made of, which factors move it the fastest, what the timeline for improvement realistically looks like, and the specific mistakes that quietly drag scores down without people realizing it.

What Your Credit Score Actually Is

In Canada, credit scores range from 300 to 900. In the US, the most commonly used FICO score ranges from 300 to 850. In the UK, each of the three main credit reference agencies uses its own scale: Experian scores from 0 to 999, Equifax from 0 to 700, and TransUnion from 0 to 710.

The number is generated by a credit bureau based on information reported by your lenders. Banks, credit card companies, auto loan providers, and mortgage lenders all report your payment behavior to one or more bureaus regularly, typically monthly.

The bureaus then run that data through a scoring model to produce a number. The higher the number, the lower the statistical risk you represent to a lender. That is all a credit score is: a numerical summary of how reliably you have handled borrowed money in the past.

Here is how the major factors break down for a FICO score, which is the most widely used model:

Payment history accounts for 35% of your score. This is whether you pay on time, every time. A single missed payment reported to the bureau can drop a good score by 60 to 110 points depending on how high it was to begin with.

Credit utilization accounts for 30%. This is the percentage of your available credit you are currently using. More on this below because it is the fastest lever most people can pull.

Length of credit history accounts for 15%. How long your accounts have been open. Older accounts help. Closing old accounts hurts.

Credit mix accounts for 10%. Having a mix of credit types, such as a credit card, a car loan, and a line of credit, is viewed more favorably than having only one type.

New credit inquiries account for 10%. Every time you apply for new credit, a hard inquiry appears on your report. Too many in a short period signals financial stress to lenders.

Canadian and UK scoring models use similar factors with slightly different weightings depending on the bureau and the specific model being used.

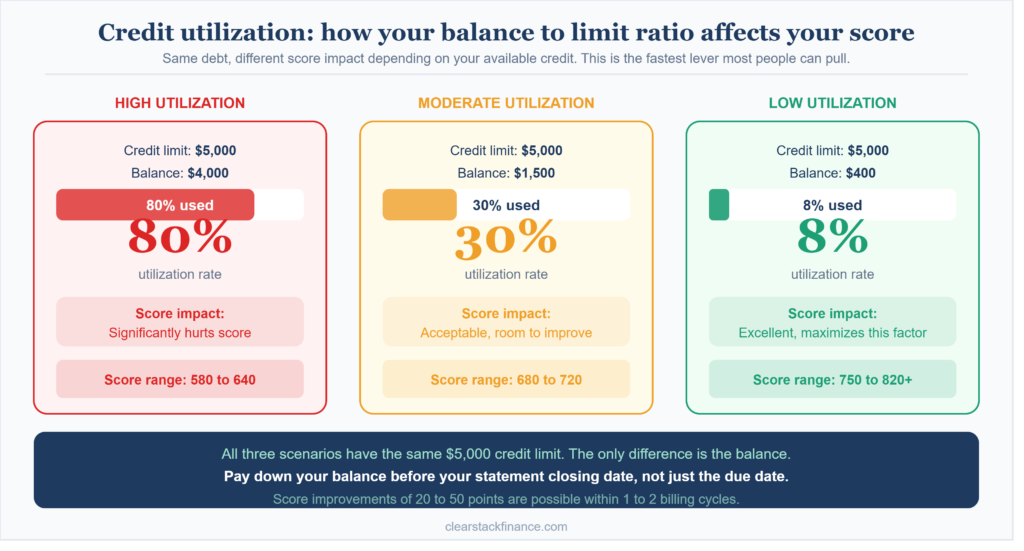

The Fastest Thing You Can Do Right Now: Fix Your Utilization

Credit utilization is the ratio of your current credit card balance to your credit limit. If your card has a $5,000 limit and you are carrying a $2,500 balance, your utilization on that card is 50%.

The general guidance you will find everywhere is to keep utilization below 30%. That is accurate but incomplete. The people with the highest scores typically keep it below 10%. The relationship between utilization and score is not a cliff at 30%, it is a slope. Lower is consistently better.

Here is the thing most people do not realize: utilization is calculated at the moment your lender reports your balance to the bureau, which is typically on your statement closing date, not your payment due date. This means even if you pay your balance in full every month, if your balance is high on the closing date, your reported utilization is high.

The practical fix: if you want to see a quick score improvement and you have a card with a high balance relative to its limit, pay it down before the statement closes rather than waiting for the due date. Some people see score improvements of 20 to 50 points within one to two billing cycles just from bringing utilization down.

If you cannot pay down the balance, there is a second option: ask your credit card company for a credit limit increase. This increases the denominator in the utilization calculation. A $2,500 balance on a $5,000 limit is 50% utilization. That same $2,500 balance on an $8,000 limit is 31%. Same debt, meaningfully different score impact.

Payment History: The Foundation You Cannot Shortcut

35% of your score is payment history. There is no trick here. You pay on time, every time, and over months and years your score reflects that.

What you can do is protect yourself from accidental late payments, which are more common than deliberate ones. A payment that slips two or three days past due because you forgot is just as damaging to your score as one you genuinely could not make.

Set up automatic minimum payments on every credit account you have. Not the full balance necessarily, just the minimum. This ensures the account is never reported as late even in a month where you are distracted or traveling. You can always pay more manually but the automatic minimum is your safety net.

If you have a late payment already on your report, the damage fades over time but does not disappear immediately. A 30-day late payment stays on your report for seven years in the US and six years in Canada, but its impact on your score diminishes significantly after the first two years of consistent on-time payments following it.

One thing worth doing if you have a single late payment with an otherwise clean history: call the lender and ask for a goodwill adjustment. This is a request for them to remove the late payment from your report as a courtesy. It does not always work and lenders are not required to do it, but it works often enough that it is worth a 10-minute phone call. The script is simple: you have been a customer for a certain number of years, you have an otherwise clean payment history, the late payment was a one-time situation, and you would like to request removal as a goodwill gesture.

The Length of Credit History Problem

This is the one that frustrates younger people most because there is no shortcut. You cannot manufacture credit history. It builds with time.

What you can do is avoid destroying it unnecessarily. The most common way people accidentally shorten their effective credit history is by closing old credit cards they no longer use.

Say you have a credit card you opened six years ago that you barely use anymore. Closing it removes that six-year-old account from your active credit mix and can shorten your average account age significantly, which hurts your score. The card also had a credit limit that was contributing to your overall available credit, so closing it raises your utilization percentage.

The better approach for a card you do not use: put a small recurring charge on it, something like a streaming subscription, and set up autopay. The account stays active and contributes positively to your history without requiring any manual management.

The exception is if the card has an annual fee that is not worth paying for a card you do not use. In that case, ask if the card can be downgraded to a no-fee version before closing it outright.

Hard Inquiries and How to Manage Them

Every time you apply for new credit, whether a credit card, a loan, a car finance agreement, or a mortgage, the lender pulls your credit report. This is called a hard inquiry and it typically drops your score by 5 to 10 points.

One or two hard inquiries in a year is normal and the impact is minor. Multiple inquiries in a short window looks to scoring models like you are desperately seeking credit, which is a risk signal.

The nuance worth knowing: for mortgage and auto loan applications specifically, multiple inquiries within a short window, typically 14 to 45 days depending on the scoring model, are treated as a single inquiry. The logic is that shopping around for the best mortgage rate is sensible consumer behavior, not a sign of financial distress. So if you are rate shopping for a car loan, do it within a concentrated period rather than spreading applications over several months.

For credit cards, this exception does not apply. Each credit card application is its own inquiry.

Errors on Your Credit Report

This is less common than credit repair companies would have you believe but it does happen and it is worth checking. Errors on your credit report, things like payments incorrectly marked as late, accounts that are not yours, or debts that have been paid but still show as outstanding, can be dragging your score down for no legitimate reason.

In Canada, you can request a free credit report from both Equifax and TransUnion once per year. In the US, you can get free reports from all three bureaus through annualcreditreport.com. In the UK, all three main credit reference agencies are legally required to provide you a free statutory report.

Go through the report line by line. Look for accounts you do not recognize, late payments you know were paid on time, balances that are listed higher than they should be, and debts that have been settled but still show as outstanding.

If you find an error, dispute it directly with the credit bureau. In Canada and the US, bureaus are required to investigate disputes within 30 days. In the UK, the timeframe is 28 days. If the investigation confirms the error, it must be corrected. Removing a legitimate error from your report can produce meaningful score improvements quickly.

What a Realistic Improvement Timeline Looks Like

This is the part most credit advice gets wrong by being either too pessimistic or falsely optimistic.

If your score is low because of high utilization and you pay down the balances, you can see improvement within one to two billing cycles. That is 30 to 60 days for a meaningful change.

If your score is low because of missed payments and you are now building a consistent on-time payment record, you are looking at six months to a year before you see substantial improvement. The late payments are still there on your report but their weight in the calculation decreases as the positive history builds up around them.

If your score is low because your credit history is short, the timeline is simply time. A year of responsible credit use adds a year to your history. There is no shortcut.

Here is a rough guide to what is realistically achievable:

Starting score in the 500 to 580 range: with consistent on-time payments, utilization below 30%, and no new negative items, most people reach the 640 to 680 range within 12 to 18 months.

Starting score in the 620 to 660 range: with utilization optimization and consistent payments, reaching 700 to 720 within 6 to 12 months is realistic for most people.

Starting score in the 680 to 720 range: breaking into the 750 and above range typically takes 12 to 24 months of clean history and low utilization, partly because at this level your history is already relatively positive and the gains come more slowly.

The Things That Will Not Help

Credit repair companies that charge monthly fees to “fix” your credit. They cannot do anything you cannot do yourself for free. They can dispute errors on your behalf, but you can dispute errors on your behalf directly with the bureau at no cost. Legitimate negative information cannot be removed by anyone regardless of what they charge you.

Closing multiple accounts to “clean up” your credit profile. This almost always backfires by reducing available credit, raising utilization, and shortening your credit history.

Opening multiple new accounts quickly to get more available credit. The hard inquiries and the lowering of your average account age will hurt more than the additional credit limit helps in the short term.

Paying off a collection account does not always remove it from your report. In Canada and the US, a paid collection still shows on your report, it just shows as paid. The account will age off after the statutory period regardless of whether it is paid. That said, some lenders will not approve applications with any unpaid collections, so paying them has practical value even if it does not help your score immediately.

Building Credit from Scratch

If you are starting with no credit history at all, the fastest path is a secured credit card. You deposit a set amount, typically $200 to $500, and that deposit becomes your credit limit. You use the card for small purchases and pay the balance in full every month. After 6 to 12 months of this, most people have enough credit history to qualify for an unsecured card.

In Canada, the Home Trust Secured Visa and the Capital One Secured Mastercard are commonly recommended entry points. In the US, the Discover it Secured and the Capital One Platinum Secured are well-regarded options. In the UK, the Vanquis Bank card and the Aqua card are popular starter options for people building credit from scratch.

Becoming an authorized user on a family member or partner’s credit card is another option. If the primary cardholder has a long history of on-time payments and low utilization, being added as an authorized user can give your credit history a meaningful boost. You do not even need to use the card for the account history to show on your report.

READ ALSO: The Subscription Trap: How to Cancel, Audit, and Take Back Control of Your Monthly Bills

Heads up: I am not a financial advisor and nothing in this article is financial advice. Credit scoring models and bureau rules vary by country and can change over time. Always verify current policies directly with the relevant credit bureaus and financial institutions in your country.

READ ALSO: How to Cut Your Grocery Bill by $150 a Month Without Eating Differently

Mike is a data analyst based in Niagara Falls, Ontario. He started ClearStack Finance after spending years figuring out personal finance the hard way. No financial jargon, no boring lectures, just practical money advice for people in their 20s and 30s who are still figuring it out.