The Grocery Problem Nobody Talks About

Groceries are the one expense that quietly bleeds most household budgets dry and nobody really notices until they sit down and add it up.

Unlike rent or car payments, there is no fixed number. The bill changes every week depending on what you grabbed, what was on sale, what you threw in the cart because it looked good in the moment, and what you eventually threw out because you forgot about it at the back of the fridge. That variability is exactly what makes it so hard to control.

The average Canadian household spends between $1,100 and $1,400 per month on food, including groceries and dining out, according to Statistics Canada data. In the US, the USDA’s moderate-cost food plan for a family of two adults aged 19 to 50 runs about $950 per month. UK households spend an average of around £60 per person per week on food according to the Office for National Statistics, which works out to roughly £240 per month for a couple.

In every case, food is typically the second or third largest household expense. And unlike rent, it is one of the few large expenses that actually has room to move without dramatically changing your life.

Cutting $150 per month from your grocery bill does not mean eating rice and beans every day. It means shopping differently. This is what that actually looks like.

Start With What You Are Actually Spending Right Now

Before anything else, go back through your last four weeks of bank and credit card statements and add up every grocery purchase. Every single one, including the small top-up shops mid-week and the corner store runs.

Most people are genuinely shocked by what they find. If you think you spend $400 a month on groceries, the real number is probably closer to $520 or $580 once you count everything. The mid-week top-up trips are where a huge amount of money quietly disappears because you go in for three things and come out with twelve.

Write the real number down. That is your baseline. Now you have something to actually measure against.

The Meal Plan is Not What You Think It Is

When most people hear “meal plan,” they picture a rigid weekly schedule with colour-coded recipes printed out on Sunday afternoon. That is not what this is.

A functional grocery meal plan is just a list of five to seven dinners you are going to make in the next week, written down before you go to the store. That is it. It does not need to be detailed. It does not need to be healthy. It just needs to exist before you leave the house.

The reason this works is simple. Without a list, you shop by impulse and whatever looks good. With a list built around actual meals, you only buy what you need. The average household throws out somewhere between 20% and 30% of the food it buys, according to research from the Food and Agriculture Organization of the United Nations. On a $500 grocery bill, that is $100 to $150 in food that goes straight into the bin.

Meal planning does not make you eat better necessarily. It just means the food you buy actually gets eaten.

A realistic starting approach: on Saturday or Sunday, spend ten minutes writing down five dinners for the week. Build your grocery list entirely around those five meals plus your usual breakfast and lunch staples. Go to the store with that list and stick to it.

The Store You Choose Matters More Than the Brands You Buy

This is the one that surprises people most and makes the biggest single difference.

There is a significant price gap between grocery store chains that most shoppers never fully appreciate because they tend to stick to one store out of habit. In Canada, shopping at Walmart Supercentre or No Frills for your staples consistently costs 20% to 35% less than shopping at Loblaws or Sobeys for the same items. In the UK, Aldi and Lidl run 30% to 40% cheaper than Tesco or Sainsbury’s on comparable products. In the US, Aldi, Walmart, and Lidl consistently undercut traditional supermarkets by a meaningful margin on everyday items.

You do not need to become a store-hopper who visits four different places every week. That wastes time and petrol. But if you are doing your main weekly shop at a premium supermarket out of habit rather than preference, switching your primary store is the highest-impact single change you can make.

A practical test: write down ten items you buy every week and check the price at your current store versus the nearest discount alternative. The difference will be obvious.

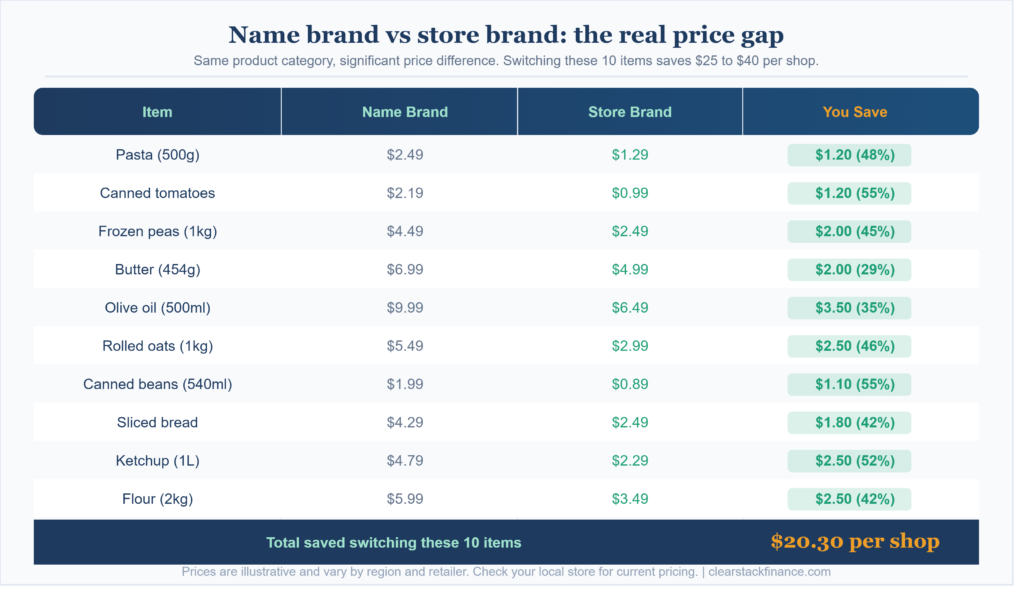

Buy the Store Brand on These Specific Things

Not everything. Some products genuinely taste different between brands and if a specific brand matters to you, keep buying it. But there is a category of groceries where the store brand is functionally identical to the name brand and costs 20% to 40% less.

These are the categories where switching to store brand almost never makes a noticeable difference:

Canned tomatoes, canned beans, and canned corn. Pasta and rice. Frozen vegetables. Butter. Eggs. Milk. Flour and sugar. Olive oil. Most condiments including ketchup, mustard, and mayo. Oats. Bread, unless you have a specific preference. Cheese for cooking. Cleaning products, though those are not groceries.

The categories where brand tends to matter more and where you should keep buying what you prefer: coffee if you are particular about it, chocolate, specific sauces with distinct flavour profiles, and anything where you have genuinely tried the store brand and found it noticeably worse.

Start by swapping just five items to store brand this week. Check if you notice a difference. Most people do not.

The Freezer Is Your Most Underused Financial Tool

Most households use their freezer for ice cream and the occasional bag of frozen peas. This is leaving money on the table every single week.

Protein is typically the most expensive part of any grocery bill. Chicken, beef, fish, and pork all freeze well and maintain quality for two to three months when properly wrapped. When these items go on sale, buying two or three weeks worth and freezing them is one of the most effective cost-saving habits you can build.

The same applies to bread. A loaf going stale does not need to go in the bin. It goes in the freezer and comes out fine for toast. Bananas going soft go in the freezer for smoothies or baking. Leftover soup, chilli, or pasta sauce freezes well and becomes a free lunch or dinner later in the week.

The practical habit: every time you open the fridge and notice something is getting close to its use-by date, freeze it before it goes bad rather than after you have already mentally written it off. This single habit alone typically saves $30 to $60 per month for a two-person household.

Shop With a Full Stomach and a Time Limit

This sounds like obvious advice but most people never actually do it, and the research behind it is solid.

A 2015 study published in JAMA Internal Medicine found that people who shopped while hungry purchased significantly more high-calorie items and spent more overall compared to when they shopped after eating. Hunger does not just make you reach for snacks. It makes you buy more of everything because scarcity-thinking affects judgment across the board when your blood sugar is low.

Beyond hunger, time pressure changes shopping behaviour. When you have a specific list and a time constraint, you move through the store efficiently and skip the browsing that leads to impulse purchases. When you have an hour and no plan, you drift.

Set a 30-minute timer when you enter the store. Build your list in store aisle order if your store layout is consistent. Get in, get what is on the list, get out. It sounds rigid but it becomes natural within a few weeks and the difference in your bill is real.

The Weekly Top-Up Trip Is Where the Budget Dies

For most households, the main weekly shop is reasonably controlled. The damage happens in the smaller top-up trips during the week.

You run out of milk on Wednesday and come back with milk, a packet of biscuits, some cheese you did not need, and a ready meal because you were tired and it was right there. That three-item run turned into $28.

The fix is not to never do a top-up shop. It is to treat it like a surgery. Go in with a list of exactly what you need. Take cash if it helps create a physical limit. Do not browse. Do not go down the snack aisle if snacks are not on your list.

Better yet, build a small buffer into your weekly shop for the predictable mid-week items you always run out of. An extra pint of milk, an extra loaf of bread. Reducing top-up trips from three per week to one saves the average household $40 to $80 per month.

Use Cashback and Loyalty Points Properly

This is not about becoming a coupon obsessive. It is about not leaving money sitting on the table that stores are actively trying to give you.

In Canada, the PC Optimum program at Loblaws and No Frills gives you points on every purchase redeemable for free groceries. Shoppers Drug Mart is included in the same program and sometimes runs 20x points events on specific products. Collecting these consistently and redeeming them on a big weekly shop every month or two is essentially a 2% to 5% rebate on everything you spend.

In the UK, Tesco Clubcard and Sainsbury’s Nectar both offer meaningful discounts on specific items each week for cardholders, sometimes significantly lower prices that are not available without the card. Using these cards every shop takes ten seconds and costs nothing.

In the US, most major grocery chains have their own loyalty apps with weekly digital coupons. Kroger, Safeway, and Publix all run these. Loading the relevant coupons before each shop takes five minutes and routinely saves $10 to $25 on a typical shop.

These programs are free. Not using them is just leaving money behind.

The Produce Strategy That Cuts Waste in Half

Fresh produce is where most grocery budgets bleed out invisibly. You buy vegetables with good intentions, life happens, and by Thursday the salad leaves are soggy and the courgettes have gone soft.

A more realistic approach for most households is a hybrid model. Buy a small amount of the fresh produce you will actually use in the first three days. Supplement with frozen vegetables for the rest of the week.

Frozen vegetables are not nutritionally inferior to fresh. In many cases they are nutritionally superior because they are frozen within hours of harvest while fresh produce may have spent days in transit and on shelves. A bag of frozen broccoli, peas, spinach, or mixed vegetables costs significantly less than fresh equivalents, lasts months in the freezer, and produces zero waste.

This does not mean never buy fresh produce. It means being realistic about what will actually get used before it spoils. Buying $15 worth of fresh vegetables and using $8 worth before the rest goes off is more expensive than buying $7 worth of frozen vegetables and using all of it.

Build a Price Memory for Your Most Common Items

Experienced grocery shoppers know roughly what things cost. This is not something you are born with, it develops over a few months of paying attention.

When you notice a “sale” on something, you need to know whether it is actually a sale or just a regularly priced item with a sale sticker. Supermarkets use pricing psychology aggressively. Items presented as deals are not always deals.

A simple habit: for the ten items you buy most frequently, write down the regular price the next time you are in the store. Keep it in your phone. After four to six weeks of shopping with that reference point, you will start to notice genuine sales versus manufactured urgency.

This matters because buying in bulk or stocking up only makes financial sense when the sale price is genuinely lower than the regular price. Buying three of something at its normal price because the display says “3 for $9” when they are regularly $2.99 each is not a saving.

What $150 Saved Per Month Actually Looks Like

Cutting $150 per month from your grocery bill sounds like a lot until you break down where it comes from.

Switching your primary store from a premium supermarket to a discount alternative on your main weekly shop: $40 to $60 per month saved.

Swapping eight to ten items to store brand: $20 to $30 per month saved.

Reducing food waste by meal planning and using the freezer properly: $30 to $50 per month saved.

Cutting mid-week top-up trips from three to one: $30 to $50 per month saved.

Using loyalty points and cashback programs consistently: $15 to $25 per month saved.

None of these individually requires you to eat differently, cook more, or spend significant time. Combined, they easily reach $150 per month for most households and often more.

The first month is the hardest because you are changing habits at the same time. By month three, most of these become automatic and you stop noticing the effort.

Heads up: I am not a financial advisor and this is not financial advice. Prices and programs mentioned here are for illustrative purposes and vary by region. Always verify current pricing and loyalty program details directly with your local retailers.

READ ALSO: Debt Avalanche vs Debt Snowball: Which Method Is Actually Better

Mike is a data analyst based in Niagara Falls, Ontario. He started ClearStack Finance after spending years figuring out personal finance the hard way. No financial jargon, no boring lectures, just practical money advice for people in their 20s and 30s who are still figuring it out.