If you have more than one debt, you have probably hit this question at some point: which one do I pay off first?

It sounds simple but it is one of the most argued topics in personal finance. Two camps, two methods, both with real results and real advocates. This article breaks down exactly how each one works, where each one wins, and which one is more likely to actually get you out of debt based on how your brain works.

The Core Difference

Both methods assume you are making minimum payments on all your debts. The difference is what you do with any extra money you can throw at debt each month.

The debt avalanche tells you to put that extra money toward the debt with the highest interest rate first, regardless of balance size.

The debt snowball tells you to put that extra money toward the debt with the smallest balance first, regardless of interest rate.

That is the whole difference. Everything else, the minimum payments, the discipline required, the timeline, flows from that one decision.

How the Debt Avalanche Works

List all your debts by interest rate, highest to lowest. Pay minimums on everything. Any extra money goes to the top of that list.

Once the highest-rate debt is gone, you take everything you were paying on it and add it to the minimum payment on the next highest-rate debt. This is called the avalanche because the payment amount grows as debts fall away.

Example:

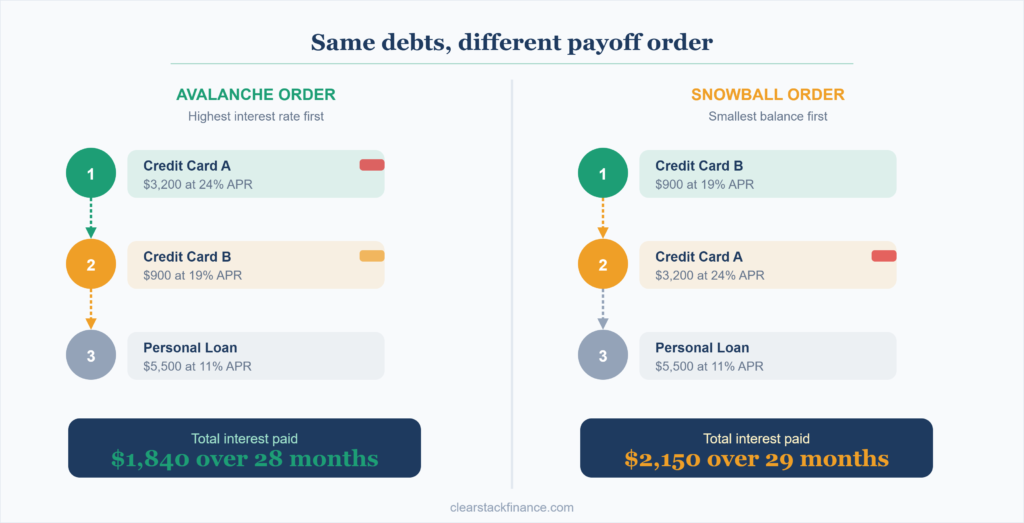

Say you have three debts:

- Credit card A: $3,200 balance at 24% interest

- Personal loan: $5,500 balance at 11% interest

- Credit card B: $900 balance at 19% interest

With the avalanche, you pay off Credit card A first (24%), then Credit card B (19%), then the personal loan (11%).

The math is clear here. You are eliminating the most expensive debt first, which means less total interest paid over the life of your repayment. If you run the numbers, the avalanche almost always saves more money than the snowball.

How the Debt Snowball Works

List all your debts by balance, smallest to largest. Pay minimums on everything. Any extra money goes toward the smallest balance.

Once that debt is gone, roll that payment into the next smallest. The payment grows as you eliminate debts, like a snowball picking up mass.

Using the same example:

- Credit card B: $900 balance at 19% interest (paid first)

- Credit card A: $3,200 balance at 24% interest (paid second)

- Personal loan: $5,500 balance at 11% interest (paid third)

Notice that Credit card B gets paid first even though it does not have the highest interest rate. You are prioritizing the quick win over the mathematically optimal order.

The Math Argument for Avalanche

If you want to minimize the total amount of money you hand over to lenders, the avalanche wins. Period.

High-interest debt is expensive. A $3,000 balance at 24% costs you $720 per year in interest if you only pay minimums. Knocking that out first stops the bleeding faster.

Across a typical debt repayment journey of two to five years, the avalanche can save hundreds to several thousand dollars depending on the interest rates and balances involved. The higher your interest rates, the bigger that gap becomes.

The Psychology Argument for Snowball

Here is where it gets interesting. The snowball should lose on paper. But a lot of people find it works better in real life.

Paying off a debt completely feels different from making progress on a large one. There is a real psychological shift that happens when you call the credit card company and close an account because the balance is zero. It builds confidence. It makes the system feel like it is working.

Research in behavioral economics backs this up. A 2016 study published in the Journal of Consumer Research found that people who focused on paying off individual accounts, rather than reducing overall debt, were more likely to eliminate their debt entirely. The motivation effect was real enough to sometimes outweigh the interest cost advantage.

Dave Ramsey built an entire financial coaching empire on this insight. His argument has always been that personal finance is more personal than it is finance. If the snowball keeps you in the game when the avalanche would have made you quit by month four, the snowball wins for you even if it loses on a spreadsheet.

Where Each Method Works Best

The avalanche is the right choice if:

- You have high-interest debt, particularly credit cards above 20%

- You are disciplined and motivated by numbers and optimization

- You can stay consistent without needing frequent visible wins

- Your debts are relatively close in balance size

The snowball is the right choice if:

- You have struggled to stick with debt payoff plans before

- You have one or two small debts you could eliminate quickly

- You find the process discouraging and need early momentum

- You know yourself well enough to know that quick wins keep you going

Some people do a hybrid. They use the snowball to knock out one or two small debts for the momentum boost, then switch to the avalanche for the rest. This is not textbook but it works for a lot of people.

What the Numbers Actually Look Like

Here is a concrete comparison using the three debts from earlier, assuming $200 per month available above minimums:

Debt avalanche total interest paid: approximately $1,840 over 28 months

Debt snowball total interest paid: approximately $2,150 over 29 months

The avalanche saves about $310 and finishes one month sooner in this example. That gap is real but it is not catastrophic. If the snowball keeps you consistent and the avalanche would have caused you to slip, that $310 difference evaporates fast.

The real cost of stopping and starting a debt payoff plan is almost always higher than the difference between these two methods.

The One Thing Both Methods Agree On

Stop adding to the debt while you pay it off.

This sounds obvious but it is the silent killer of both methods. If you are paying $200 extra per month toward debt but putting $150 per month of new spending on a credit card, the math falls apart. You are running up a hill on a treadmill.

Before picking a method, look honestly at your spending and make sure you are not actively making the pile bigger. A rough budget, even a simple one, needs to be in place alongside whichever payoff method you choose.

Which One Should You Pick

Honestly, the best method is the one you will actually stick with.

If you are someone who tracks spreadsheets and gets satisfaction from watching total interest go down, use the avalanche. If you need to see accounts close and feel progress in a tangible way, use the snowball.

Run your numbers both ways using a free debt payoff calculator. Undebt.it is a good free tool that lets you compare both methods side by side with your actual balances and interest rates. Look at the difference in total interest and ask yourself honestly whether that amount justifies using the method you find harder to stick with.

Most of the time the answer is no. A slightly more expensive method you actually finish beats a mathematically perfect plan you abandon.

Heads up: I am not a financial advisor and nothing in this article is financial advice. Always talk to a qualified professional before making decisions about your debt repayment strategy.

Mike is a data analyst based in Niagara Falls, Ontario. He started ClearStack Finance after spending years figuring out personal finance the hard way. No financial jargon, no boring lectures, just practical money advice for people in their 20s and 30s who are still figuring it out.