Most budgets fail within two weeks. Not because people are bad with money, but because the budget they built had no real structure. It was basically just a list of expenses they hoped they could stick to, with no system behind it.

Zero-based budgeting is different. It is one of the few methods that actually forces you to think about every dollar you earn before you spend it. And once you set it up properly, it works whether you make $2,800 a month or $8,000 a month.

This guide walks you through the whole thing from scratch. No fluff, no vague advice about “cutting lattes.” Just the actual system.

What Zero-Based Budgeting Actually Means

The idea is straightforward. Every dollar you earn gets assigned a job before the month starts. By the time you are done building the budget, your income minus your expenses equals zero.

That does not mean you spend everything. It means every dollar is accounted for, including the ones going into savings, investments, or an emergency fund. You are telling your money where to go rather than wondering where it went.

The concept was popularized by Dave Ramsey, though variations of it have existed in corporate finance for decades. For personal use, it works because it removes the vagueness that kills most budgets. “I’ll try to spend less on food this month” is not a plan. “$400 on groceries, not a dollar more” is a plan.

Why Most Budgets Do Not Work

Before getting into the how, it helps to understand why the typical approach fails.

Most people build what is essentially a spending estimate. They look at last month’s bank statement, round some numbers, write down categories, and call it a budget. The problem is there is no accountability built in. If you go $60 over on dining out, nothing stops you. Nothing even flags it until you check your statement three weeks later.

Zero-based budgeting creates friction in the right places. When you have already assigned that $60 to something else, overspending on restaurants means actively taking money from another category. That decision feels different when it is concrete.

What You Need Before You Start

You do not need any special software. A spreadsheet works. A notebook works. There are also free apps like YNAB (paid, but worth it for some people) and EveryDollar that are built specifically for this method. For your first month, a Google Sheet is fine.

What you actually need:

Your total monthly take-home income. Not gross salary, the amount that actually hits your bank account after taxes and deductions. If your income varies month to month, use your lowest average month as the baseline. You can always adjust upward if you earn more.

Three months of bank and credit card statements. You need these to understand what you actually spend, not what you think you spend. There is almost always a gap between the two.

About an hour to set things up the first time. After that, monthly reviews take 20 to 30 minutes.

Step 1: Calculate Your Real Monthly Income

Add up everything that comes in each month after tax. Employment income, side hustle income, any consistent transfers or support payments. Write down one number.

If you are salaried, this is straightforward. If you freelance or do shift work, average the last three months and use the lower end of that range. The goal is to build a budget around what you can count on, not your best month.

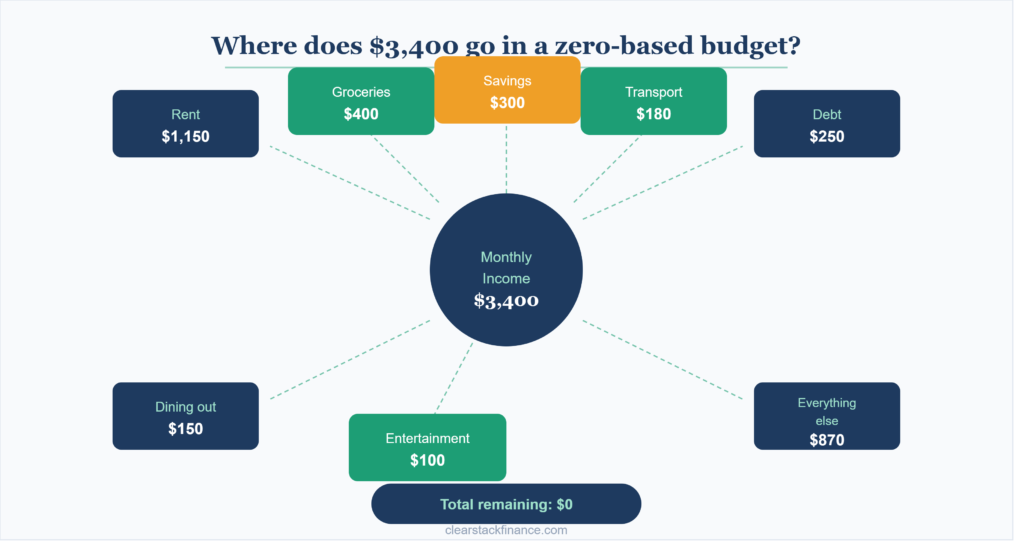

For example: if your take-home is $3,400 per month, that is your starting number. Everything else in the budget has to fit inside that $3,400.

Step 2: List Your Fixed Expenses First

Fixed expenses are the ones that do not change month to month. Rent or mortgage, car payment, insurance premiums, internet bill, phone plan, minimum debt payments. These go into the budget first because they are non-negotiable.

Write them all down with the exact amounts. If your rent is $1,150, write $1,150, not “around $1,200.” Precision matters here.

Once your fixed expenses are listed, subtract them from your income. Using the $3,400 example, if fixed expenses total $1,800, you now have $1,600 left to work with.

Step 3: Estimate Your Variable Expenses

Variable expenses are the ones that fluctuate: groceries, gas, dining out, entertainment, clothing, personal care. This is where most people underestimate badly.

Go through your last three bank statements and calculate what you actually spent in each category. The numbers will probably surprise you. People consistently underestimate grocery spending by 20 to 40 percent and dining out by even more.

Set realistic numbers based on your actual history, then decide where you want to trim. The key word is realistic. A budget that requires you to cut grocery spending from $600 to $200 is not a plan, it is wishful thinking.

Common variable categories to account for:

- Groceries

- Dining out and takeaway

- Gas or transit

- Personal care (haircuts, products)

- Clothing

- Entertainment and subscriptions

- Household supplies

- Gifts and social spending

Step 4: Include Savings and Irregular Expenses

This is the step most budgets skip, and it is why people end up in trouble when the car needs new tires or a birthday comes up.

Savings goes into the budget as a fixed line item, not whatever is left over at the end of the month. If you want to save $300 per month, it gets written in like a bill you pay yourself first.

Irregular expenses need to be broken down monthly. If you spend roughly $600 per year on car maintenance, that is $50 per month. Write that in. Annual subscriptions, holiday gifts, back-to-school expenses, annual insurance premiums: divide them by 12 and budget for them monthly. When the expense comes up, the money is already sitting there.

Step 5: Make It Equal Zero

Now add everything up: fixed expenses, variable expenses, savings, irregular expense allocations. Subtract the total from your income.

If the number is negative, you are planning to spend more than you earn. Go back through each category and cut until you reach zero. Start with variable categories and extras before touching fixed costs.

If the number is positive, you have unallocated money. This is not a win, it is an oversight. Put that money somewhere specific: extra debt payment, higher savings contribution, a sinking fund for something you need. Do not leave it floating.

The goal is income minus all allocations equals exactly zero.

The First Month Will Be Wrong

Accept this now. Your first zero-based budget will have estimates that are off. You will forget a category. Something unexpected will come up.

That is not failure, it is data. At the end of month one, go through your actual spending versus what you budgeted and note where the gaps were. Adjust month two accordingly.

Most people find that it takes two to three months before the budget starts feeling accurate and natural. By month three, you will know your numbers well enough that the setup takes about 15 minutes.

Handling Irregular Income

If your income varies, the zero-based method still works but the approach changes slightly.

Budget based on your minimum expected income for the month. If you earn more, hold the extra until you know the full month’s income, then assign it during a mid-month check-in. You can put surplus toward debt payoff, savings, or upcoming large expenses.

The key is not to spend ahead of income you have not earned yet. Build the budget around what you know is coming, not what you hope might arrive.

The Difference Between Zero-Based and Zero-Balance

A common misunderstanding: zero-based does not mean your bank account hits zero. Your emergency fund, savings accounts, and investment contributions are all budget categories. Money assigned to savings is not “spent,” it is allocated.

Your chequing or checking account should still have a small buffer at all times to avoid overdrafts and banking fees. Many people who use this method keep $100 to $200 as a permanent buffer that they do not count as available income.

Common Mistakes That Kill the Budget

Forgetting about subscriptions. Go through your bank and credit card statements specifically looking for recurring charges. Streaming services, gym memberships, app subscriptions, cloud storage: add them all. These small amounts accumulate fast and are easy to overlook.

Not budgeting for fun. A budget with no money allocated for entertainment or dining out is a budget you will abandon. Give yourself a realistic amount for enjoyment. The goal is not misery, it is control.

Setting categories too broadly. “Miscellaneous: $200” is not useful. Break it down. The more specific your categories, the more honest your budget is.

Only looking at it once. Your budget needs a weekly check-in, especially in the first few months. Five minutes on Sunday reviewing the week keeps you aware before problems compound.

Tools That Make This Easier

You do not need to pay for anything to do this well. Google Sheets has free budget templates that work perfectly. Search “zero based budget Google Sheets template” and you will find dozens.

If you want an app, EveryDollar has a free version built specifically for zero-based budgeting. YNAB (You Need a Budget) is the most powerful option and is worth the cost if you have complicated finances or irregular income, but it is not necessary to start.

The best tool is whichever one you will actually open and use regularly. A spreadsheet you check weekly beats a sophisticated app you look at once a month.

What Happens After the First Three Months

Once the budget feels accurate and you have adjusted the categories to match reality, you will start noticing things shift. Spending decisions feel more deliberate. You know exactly where your money is going. Impulse purchases feel different when you have to decide which category to take the money from.

Some people find they can save significantly more than they expected once the budget reveals where money was quietly disappearing. Others find they were actually doing fine and just needed more visibility to feel secure.

Either outcome is useful.

Heads up: I am not a financial advisor and nothing in this article is financial advice. This is based on research and personal experience. Before making any significant financial changes, talk to a professional who knows your specific situation.

Mike is a data analyst based in Niagara Falls, Ontario. He started ClearStack Finance after spending years figuring out personal finance the hard way. No financial jargon, no boring lectures, just practical money advice for people in their 20s and 30s who are still figuring it out.