Let me tell you something nobody puts in their investing guide.

The first time I bought a stock, I spent four hours reading about a company, convinced myself I understood the business, bought $200 worth of shares at 11pm on a Tuesday, and checked the price 47 times the next day. It dropped 6% by Thursday. I sold it. It went up 23% the following month.

That is not a cautionary tale about stock picking. That is what happens when someone who has never invested before tries to learn by doing without understanding the actual rules of the game first.

This article is for the person who knows they should be investing, has maybe $50 to $500 sitting there doing nothing, and has no idea where to actually start without making the same dumb mistakes I did.

Everything here is factually accurate. Some of it you will not find explained this way anywhere else because most investing guides are written for people who already understand the basics. This one is not.

Why Most Beginners Start Wrong

The typical beginner investing journey goes something like this. You hear someone talk about investing. You feel behind. You open a brokerage account because you heard it was a good idea. You stare at it. You do not know what to buy. You either buy something random based on a Reddit post or you do nothing and the account sits empty for six months.

Both of those outcomes are more common than anyone admits.

The problem is not lack of motivation. The problem is that most investing content skips the part where they explain what you are actually doing when you invest. Not the mechanics, the actual concept.

So before anything else, here is the real explanation.

What You Are Actually Doing When You Invest

When you buy a share of a company, you are buying a small ownership stake in that business. If the business grows and becomes more valuable over time, your stake becomes more valuable too. If it shrinks, so does your investment.

When you buy an index fund, you are buying a tiny piece of hundreds or thousands of companies at once. You are not betting on one company. You are betting that the overall economy will be worth more in 10 years than it is today. Historically, across every major economy, that bet has been right.

That is the whole thing. Everything else is detail.

The reason this matters before you open an account is that it changes how you think about short-term price movements. When the market drops 15% in a month, which it does regularly and will keep doing, someone who understands what they own stays calm. Someone who does not understands they own numbers on a screen that are currently smaller, which is terrifying.

The Account You Open Matters More Than What You Buy

This is the part that took me personally about eight months to figure out, and I have never seen it explained clearly for beginners.

Before you decide what to invest in, you need to decide where to hold those investments. The account type determines how your money is taxed, which over 20 or 30 years makes an enormous difference.

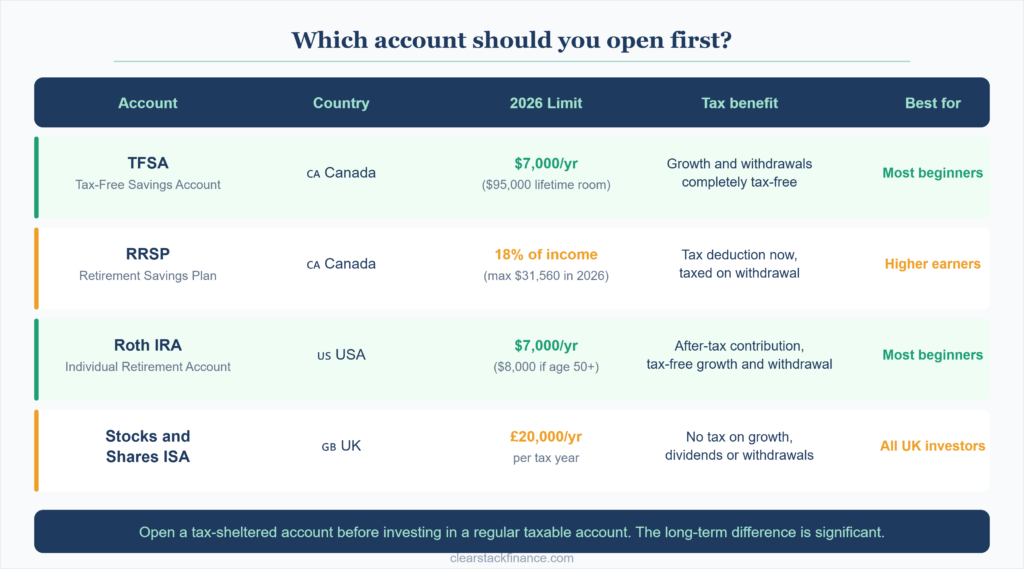

In Canada, the two accounts you need to know about are the TFSA and the RRSP.

The Tax-Free Savings Account (TFSA) lets you invest and withdraw money completely tax-free. Any growth inside a TFSA, whether from dividends, interest, or the investment increasing in value, is yours to keep without paying tax on it when you take it out. As of 2026, the cumulative TFSA contribution room for someone who has been eligible since 2009 is $95,000. If you have never contributed, that room is sitting there waiting.

The Registered Retirement Savings Plan (RRSP) gives you a tax deduction now. You contribute pre-tax money, it grows tax-sheltered, and you pay tax when you withdraw in retirement. The logic is that you earn more now than you will in retirement, so you pay less tax overall.

For most people in their 20s and 30s who are just starting out, the TFSA is the right first account. It is flexible, there is no penalty for withdrawing, and the tax-free growth compounds beautifully over decades.

In the United States, the equivalent is a Roth IRA. You contribute after-tax money and it grows tax-free. The 2026 contribution limit is $7,000 per year, or $8,000 if you are over 50. Like the TFSA, this is where most young investors should start.

In the UK, the Stocks and Shares ISA works similarly. You can invest up to £20,000 per tax year and pay no tax on growth or withdrawals.

Open one of these before you do anything else. Investing inside a regular taxable account when you have unused room in a tax-sheltered account is one of the most common and most costly beginner mistakes.

The $100 Question: Is It Even Worth It

Yes. Not because $100 will make you rich, but because the habit and the education you get from actually having money in the market are worth more than the $100 itself.

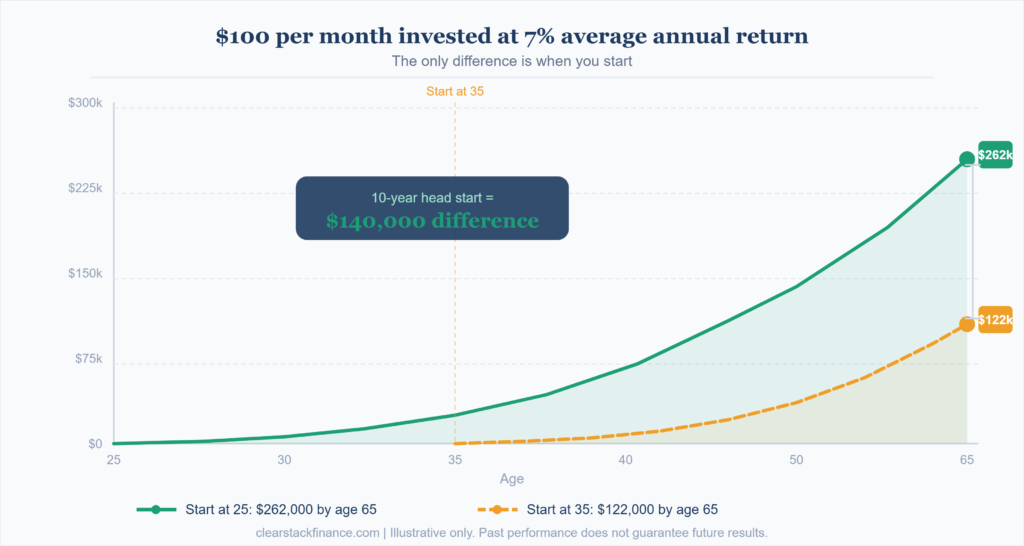

Here is the math that actually matters. If you invest $100 per month starting at 25 into a low-cost index fund that returns an average of 7% annually, you will have approximately $262,000 by age 65. That same $100 per month started at 35 produces about $122,000 by 65. The 10-year head start is worth $140,000, and you only contributed $12,000 more to get it.

The point is not the $100. The point is starting.

That said, there is one thing to sort out before you invest anything: high-interest debt. If you have credit card debt at 20% or above, paying that off first is mathematically a better return than any investment you can make. A guaranteed 20% return by eliminating debt beats a probable 7% return in the market every time.

Once the high-interest debt is gone, or if you do not have any, you are ready to invest.

What to Actually Buy When You Are Starting With a Small Amount

This is where most beginner guides get vague. They say things like “consider low-cost index funds” and then list ten options without telling you how to choose between them.

Here is a concrete starting point based on where you live.

If you are in Canada and opening a TFSA, look at XEQT or VEQT. These are all-in-one equity ETFs available on the Toronto Stock Exchange. XEQT is managed by BlackRock’s iShares and VEQT is from Vanguard. Both hold thousands of companies across Canada, the US, and internationally in a single fund. Management fees are around 0.20% per year, which is extremely low. You buy one fund, you are diversified across the global economy. You do not need to rebalance. You do not need to think about it month to month.

If you are in the US and opening a Roth IRA, look at VTI (Vanguard Total Stock Market ETF) or FZROX (Fidelity Zero Total Market Index Fund, which has zero management fees). Both give you exposure to the entire US stock market in one purchase.

If you are in the UK and opening a Stocks and Shares ISA, look at the Vanguard FTSE Global All Cap Index Fund or the iShares Core MSCI World ETF. Both are available through platforms like Vanguard UK directly, Hargreaves Lansdown, or Freetrade.

The common thread across all of these: low fees, broad diversification, no need to pick individual companies. You are buying the market, not betting on it.

The Mistake That Cost Me Real Money

I want to tell you about the specific thing I got wrong because I have never seen it explained in a way that actually registers for beginners.

After my initial disaster with individual stocks, I opened a proper account and bought an index fund. Great. I was doing it right. Then the market dropped about 18% over a few months. My $800 investment was worth about $656. I felt sick. I sold it.

Three months later the market had recovered completely and was higher than when I bought in. If I had done nothing, I would have been fine.

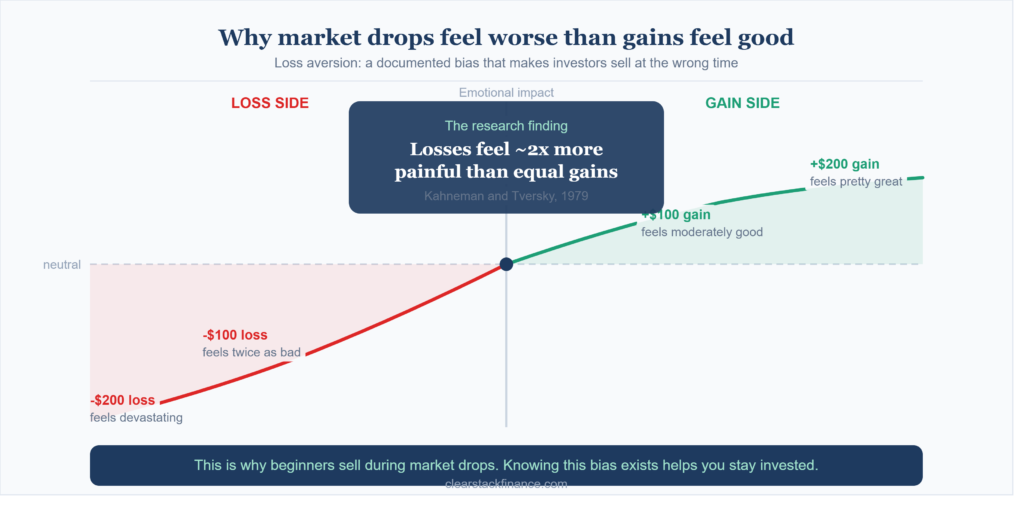

The selling during a downturn is the single most damaging thing a beginning investor can do, and almost every beginner does it at least once. The reason is that a paper loss feels more real than an unrealized gain. Seeing your balance drop from $800 to $656 triggers the same emotional response as losing $144 in cash, even though you have not actually lost anything until you sell.

The technical term for this is loss aversion, and it is well-documented in behavioral economics going back to Kahneman and Tversky’s work in the 1970s. The loss feels roughly twice as painful as an equivalent gain feels good.

Knowing this does not make it easier in the moment. What does help is understanding that market downturns are not anomalies. They are scheduled events that happen without a schedule. Since 1950, the US stock market has experienced a drop of 10% or more roughly every 16 months on average. It has always recovered.

The strategy is not to predict when drops happen. It is to be invested in something broad and low-cost enough that you can survive them without panicking.

How Often Should You Check Your Investments

This is a question I never see answered directly in beginner guides, so here is a direct answer.

Once a month maximum in the first year. Once a quarter after that.

Checking your investment account daily is not engagement, it is anxiety. The value of a long-term index fund investment on any given Tuesday is completely irrelevant to your financial outcome in 20 years. The only number that matters is the one when you need the money.

If you are using your brokerage’s mobile app and you are opening it more than once a week, turn off the push notifications and move the app off your home screen. This is not a joke. Frequent checking leads to emotional decisions and emotional decisions cost money.

Set up automatic contributions if your brokerage allows it. Decide on an amount you can consistently invest each month, set the transfer to happen automatically, and then largely ignore it. This is called dollar-cost averaging and it means you buy more shares when prices are low and fewer when prices are high, which over time produces a reasonable average cost per share without requiring you to time anything.

The Platforms Worth Looking At

In Canada: Questrade and Wealthsimple Trade are the two most popular options for beginners. Wealthsimple has no commission on ETF purchases and a clean app that is easy to navigate. Questrade charges a small fee to buy but nothing to sell ETFs. Both offer TFSA and RRSP accounts.

In the US: Fidelity and Charles Schwab are the two strongest options for beginners. Both have no account minimums, no trading commissions, and strong educational resources. Fidelity has fractional shares which means you can buy partial shares of expensive ETFs with small amounts.

In the UK: Vanguard UK is the cleanest starting point if you want to keep things simple and stay with their funds. Freetrade is good for beginners who want commission-free trading with a modern app. Hargreaves Lansdown is more established and has stronger research tools but charges slightly more.

Avoid platforms that push you toward options trading, crypto, or leveraged products as a beginner. These are not investments, they are speculation, and they are specifically designed to be more engaging and more dangerous than index fund investing.

What Happens in the First 90 Days

Month 1: You open the account. It feels anticlimactic. You buy your first ETF. The number goes up slightly, then down slightly. Nothing dramatic happens. This is correct.

Month 2: You contribute again. You notice your total invested is growing but the market value fluctuates daily. You check it more than you should. This is normal.

Month 3: Either the market has gone up and you feel smart, or it has gone down and you feel anxious. Either way, you do nothing. You make your contribution. You close the app.

That is what successful beginning investing actually looks like. It is boring on purpose. The excitement is for the finish line, not the process.

One Number to Keep in Mind

The average annual return of a globally diversified index fund over any 20-year period in modern market history has never been negative. Not once. Not even including periods that started right before the 2008 financial crisis or the dot-com crash.

That is not a guarantee of future performance. Nothing is. But it is a reason to stay in the game when it feels uncomfortable.

Your job as a beginning investor is simple. Open the right account. Buy something broad and cheap. Contribute consistently. Do not sell when it drops. Leave it alone.

Everything else is noise.

Heads up: I am not a financial advisor and nothing in this article is financial advice. The specific products and platforms mentioned here are for informational purposes only. Always do your own research and speak to a qualified financial professional before making investment decisions. Tax rules and contribution limits change, so verify current figures with official government sources or a licensed advisor in your country.

Also, read about How to Build a Zero-Based Budget

Mike is a data analyst based in Niagara Falls, Ontario. He started ClearStack Finance after spending years figuring out personal finance the hard way. No financial jargon, no boring lectures, just practical money advice for people in their 20s and 30s who are still figuring it out.